Coachability: The One Trait That Predicts Management Team Success

Sit through enough PE management interviews and a pattern surfaces.

The frameworks for everything else are sophisticated. Quality of earnings packages running 80 pages. Industry experts on retainer. Customer reference checks for every top-20 account. Models with fifty tabs and assumptions tested against benchmarks. Then the conversation turns to the people running the company, and the assessment collapses to a single binary. Coachable. Or not.

Gretchen Perkins, partner at Avance Investment Management, opens management interviews with that same first question: are they coachable? Not the deepest question, not the most sophisticated. Just the first one. It’s almost embarrassing how simple it is. It’s also probably the highest-leverage call you’ll make in the whole deal.

What “Coachable” Actually Means

Coachability isn’t politeness. It isn’t agreement. It isn’t a CEO who nods through every operating review and then does whatever they were already going to do. That’s the worst version — performative coachability. The hardest type to spot in diligence and the most expensive after close.

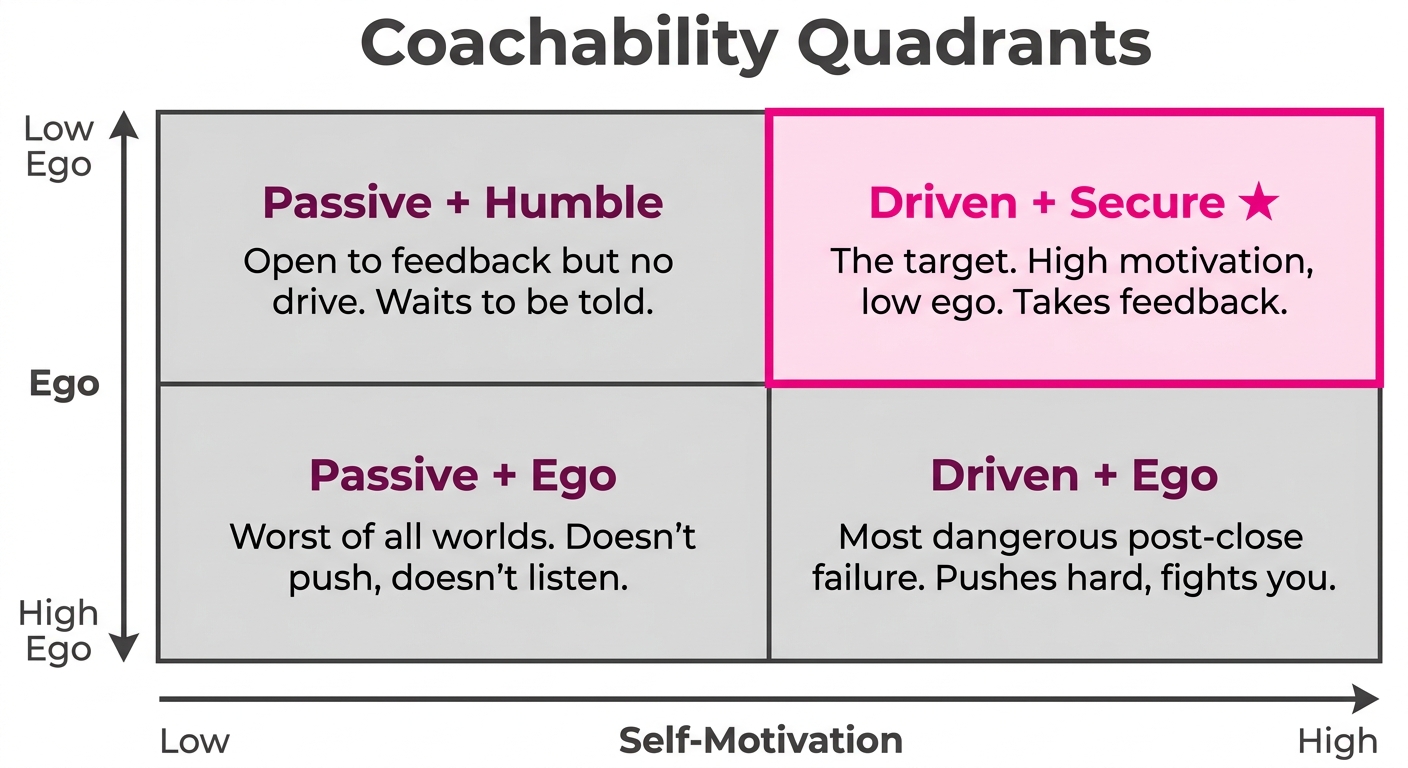

Real coachability has a specific shape. John Hodge at Rubicon Founders calls it “self motivation without ego.” That phrase is doing more work than it looks. Self-motivation means the operator drives themselves — they don’t need a board to tell them what’s broken. Without ego means they can hear that something is broken without treating the message as a personal attack.

The combination is rare. Operators with self-motivation often have ego. They built the thing. They’re proud of what they built. Operators without ego often lack drive. They wait to be told. The intersection — driven enough to push, secure enough to listen — is the trait you’re looking for.

You’ve sat across from this person. You’ve also sat across from the opposite. The opposite talks more, knows more, defends more, and learns less.

Why This Matters More Than the Org Chart

PE firms exist to add value. The pitch deck says it. The LP letters say it. The whole thesis assumes it. Operating partners run playbooks. Pricing studies. Sales force effectiveness. ERP rollouts. Procurement consolidation. Pick your initiative.

None of it works if the operator on the other end is fighting you.

Devin Mathews at ParkerGale Capital frames the partnership question in a way that sticks. “We could do it with people rather than to people,” he says — which sounds soft until you sit with it. The PE firm has a choice every day: collaborate, or impose. Coachable teams enable the first. Uncoachable teams force the second. And once you’ve started doing it to people, the value creation plan turns into a compliance exercise. Reports get filed. Initiatives get launched. Nothing actually moves.

Vinay Kashyap at Mainsail Partners hears the same thing from his coachable founders, framed as a benefit. “We don’t want to pay the dumb tax,” is how one of them put it to him. They want the institutional knowledge. They want the benchmarks from forty other software businesses Mainsail has touched. They want to skip the avoidable mistakes the PE firm has already watched other portcos make.

That’s coachability speaking, in the operator’s own words. I know I don’t know everything. I’d rather not learn the expensive way.

The flip side is what every uncoachable management team says — sometimes out loud, more often through behavior. I’ve been doing this for 15 years. You bought my company. I don’t need your benchmarks. Both stances are common. One generates returns. One drains them.

Diligence Validates the Spreadsheet, Not the Person

Here’s the structural problem. Diligence validates the spreadsheet, not how the business works — and even less how the people running it will respond when you tell them something they don’t want to hear.

Reference calls catch it sometimes. A former boss who says “she’s great, very talented, but she had her own way of doing things” is telling you exactly what you need to hear, in code. Most of the time, though, references are sourced by the seller and pre-screened to say complimentary things. They tell you the operator is smart, hard-working, and well-liked. They don’t tell you whether that operator can be told they’re wrong.

Management presentations are even worse. A founder selling their company is performing. They’ve been coached by the banker, dressed by the spouse, and rehearsed by their CFO. Of course they smile and engage. Of course they say “we’d love a partner.” That’s the script. You’re not seeing the operator. You’re seeing the version of the operator the deal team has packaged for sale.

What you actually need is a real-time test. Not a prepared answer. A response.

Share a contrarian perspective during diligence. Push back on something the management team is proud of. Tell them you think a flagship initiative they ran last year was probably a mistake — and watch their face.

Coachable operators get curious. Tell me more — what did you see that we missed? They lean in. They ask follow-up questions. They might disagree, but they engage with the substance.

Uncoachable operators get defensive. You don’t understand our market. That isn’t how it works here. We’ve already considered that. The substance goes untouched. The defense is the whole response.

The point isn’t whether you’re correct about the contrarian view. The point is what they do when challenged. The response IS the assessment.

Character Beats the Tech Stack

There’s a tendency in PE — especially in tech-heavy verticals — to treat operator assessment as a secondary problem. The thinking goes: we’ll buy the company, modernize the systems, install the dashboards, professionalize the reporting, and the management quality issues will surface on their own. The platform will reveal the people.

It doesn’t work that way. Tech enablement does not equal analytics capability — and analytics capability does not equal a leadership team that can absorb what the analytics tell them. We’ve made the data-access version of this argument — how the seller and the management team respond to “show me how a unit gets made” is itself the coachability test, before any dashboard exists.

Jessica Ginsberg at LFM Capital says it more directly. “You can have the best ERP system. You can have the most automated facility, but if you don’t have the right person at the top, it doesn’t matter.”

She’s not anti-technology. LFM invests in industrial businesses where systems matter. She’s making a hierarchy claim: leadership quality sits above the tech stack, not next to it. Put a coachable CEO in a company with mediocre systems and you’ll improve the systems. Put an uncoachable CEO in a company with best-in-class systems and you’ll still miss the plan, because nobody is willing to act on what the dashboards show.

The upside case is just as concrete. Engaged teams generate effort that doesn’t show up on any org chart or comp plan — they push through friction the playbook didn’t anticipate. Disengaged teams move at exactly the pace required to keep their jobs, and not a step faster.

At sub-250 employee scale — typical PE portco territory — the CEO touches everyone. Their coachability becomes the company’s coachability within 12 months, because culture follows leadership at that size. Whatever the CEO models, the team mirrors. If the CEO treats the PE firm as a partner, the team does too. If the CEO treats them as outsiders, the team falls in line.

Making Coachability a Diligence Discipline

If coachability is the highest-leverage call in the deal, it should be a formal part of how you assess management. Not a hallway impression. Not a gut read after the bake-off. A discipline.

A few ways to build it in:

Run a contrarian session during diligence. Not a hostile one. A real exchange where you bring a perspective the management team hasn’t heard — preferably one informed by what you’ve seen at comparable portfolio companies — and observe how they respond over the next 60 minutes. Not just the initial reaction. The whole arc. Do they come back to it? Do they ask follow-up questions in the next call? Or do they pretend the conversation didn’t happen?

Ask about a past mistake. Not the rehearsed one (“we hired too fast in 2022”). A real one. What’s something you got wrong in the last 18 months, what did you learn, and what would you do differently? Coachable operators have answers. Uncoachable operators have excuses framed as answers.

Reference-check for the trait specifically. Most reference questions cover competence and culture fit. Add coachability. Tell me about a time this person had to change their mind about something important. How did they handle being wrong? Who do they take advice from? The answers cluster.

Watch how they handle their own team’s criticism. Sit in on an internal meeting if you can. Not the one staged for you. A real one. Does the CEO welcome dissent or shut it down? Does the team push back, or does everyone agree with the boss? The behavior in the room is the data.

None of this requires a new framework. It requires treating character as something you actually assess, not something you note in passing.

Stakes

Two deals with similar financial profiles, similar markets, similar capital structures. Coachable management on one. Defensive management on the other. The first deal compounds — every quarter, the team absorbs feedback, executes initiatives, and moves the operating metrics in the direction the value creation plan needs them to go. The second deal stalls. Every initiative hits friction. Every operating review becomes a debate. Every benchmark the PE firm shares gets dismissed as “not applicable to our business.”

Same model. Same playbook. Different people. Different outcomes.

You bought a company. The financials told you what it was worth on paper. The people will tell you what it’s actually going to return.

If you’re building a diligence process that takes coachability seriously — moving it from gut-check to discipline — that’s exactly the kind of work I do.

Alex Escoriaza helps PE firms and operators figure out what they’ve actually bought — including how the people running the company will respond when reality reveals the gaps. If you’re sharpening management assessment for the next deal, reach out.