The Era of Financial Engineering Is Over — Why Operational DD Is No Longer Optional

PE runs four types of due diligence on every deal.

Financial. Commercial. Legal. Tax.

There’s a fifth type. It’s the one that would have told you whether the business can actually execute a value creation plan. Most firms still skip it. And for most of the last fifteen years, skipping it didn’t cost them much — because the returns came from somewhere else entirely.

That somewhere else is gone.

The Math That Made Operational DD Optional

McKinsey’s analysis of PE returns from 2010 to 2021 is uncomfortable reading if you’re honest about it. Roughly two-thirds of returns during that period came from two sources: financial leverage and multiple expansion. (McKinsey, “Bridging Private Equity’s Value Creation Gap,” 2024.)

Put plainly: for over a decade, PE firms could buy a decent business, lever it up, ride a multiple expansion cycle, and exit at a premium — without ever needing to deeply understand how the operations worked. The model rewarded deal execution and timing. It didn’t reward operational insight.

This isn’t a criticism. It was rational. Why build an expensive operational assessment capability when financial engineering is doing most of the work?

But rates normalized. Multiples compressed. The easy decade is over.

The remaining third of returns — the ones that came from actual operational improvement — are now the only reliable driver left. And that changes what due diligence is for.

The DD Stack PE Built for a Different Era

Walk through any serious PE firm’s diligence process and you’ll find something impressive. Quality of Earnings reports that dissect revenue recognition down to contract terms. Commercial due diligence that maps TAM, competitive positioning, and customer concentration risk. Legal review that identifies every liability that might survive a deal. Tax structuring that optimizes the capital structure before close.

These workstreams are rigorous, expensive, and all asking versions of the same question: Is the financial story real?

What none of them answer is: Can this business actually improve?

That’s a different question — one operational assessment is built to answer. And here’s what makes it so easy to skip: unlike financial or commercial diligence, operational assessment doesn’t have a standardized deliverable. There’s no ODD equivalent of a QofE report that every PE firm knows how to read and price. So it gets deferred — to the first 90 days post-close, to the newly hired operating partner, to intuition about the management team. We cover how that gap surfaces after the close in detail elsewhere, but the pattern is consistent: the assessment gets pushed to the moment when it’s already too late to change the price you paid.

PE operators put it plainly: “Move beyond the spreadsheets and find the real bottlenecks.” That’s not sophisticated advice. It’s basic. And yet it describes exactly what most diligence processes don’t do.

What 70 Operators Wish They’d Been Asked

The clearest evidence for the ODD gap isn’t from PE firms looking back. It’s from the operators who lived through the close without it.

Across 70 acquisition accounts, the pattern is consistent: operators who understood the financial model going in still got surprised — not by the numbers, but by the operations. Wrong priorities. Team capacity that looked fine on paper and wasn’t. Seller psychology nobody thought to assess. Revenue streams that looked profitable at the consolidated level and weren’t at the unit level.

None of those things are in the QofE. They’re not in the CIM. When you aggregate what operators keep getting wrong, it stops looking like individual error and starts looking like a structural gap in what diligence is built to find.

What Diligence Validates vs. What It Doesn’t

The core issue is this: standard diligence validates that a business exists in a certain financial state. It doesn’t validate whether the business can improve from that state.

That distinction matters more now than it did in 2015.

John Caple, a PE investor, frames the opportunity clearly: “Literally the easiest value lever PE pulls is understanding that different kinds of cash flows have very different multiples.” Per-service-line profitability. Revenue stream durability. The gross margin differential between your best and worst customer segments. These aren’t exotic insights — but you can only act on them if you’ve assessed the operations pre-close and know which revenue streams are worth improving.

Diligence validates the spreadsheet. It doesn’t validate how the business works.

The QofE tells you the EBITDA is real. Operational due diligence tells you whether you can grow it — or even sustain it — under new ownership. Without both, you’re buying a financial model, not a business.

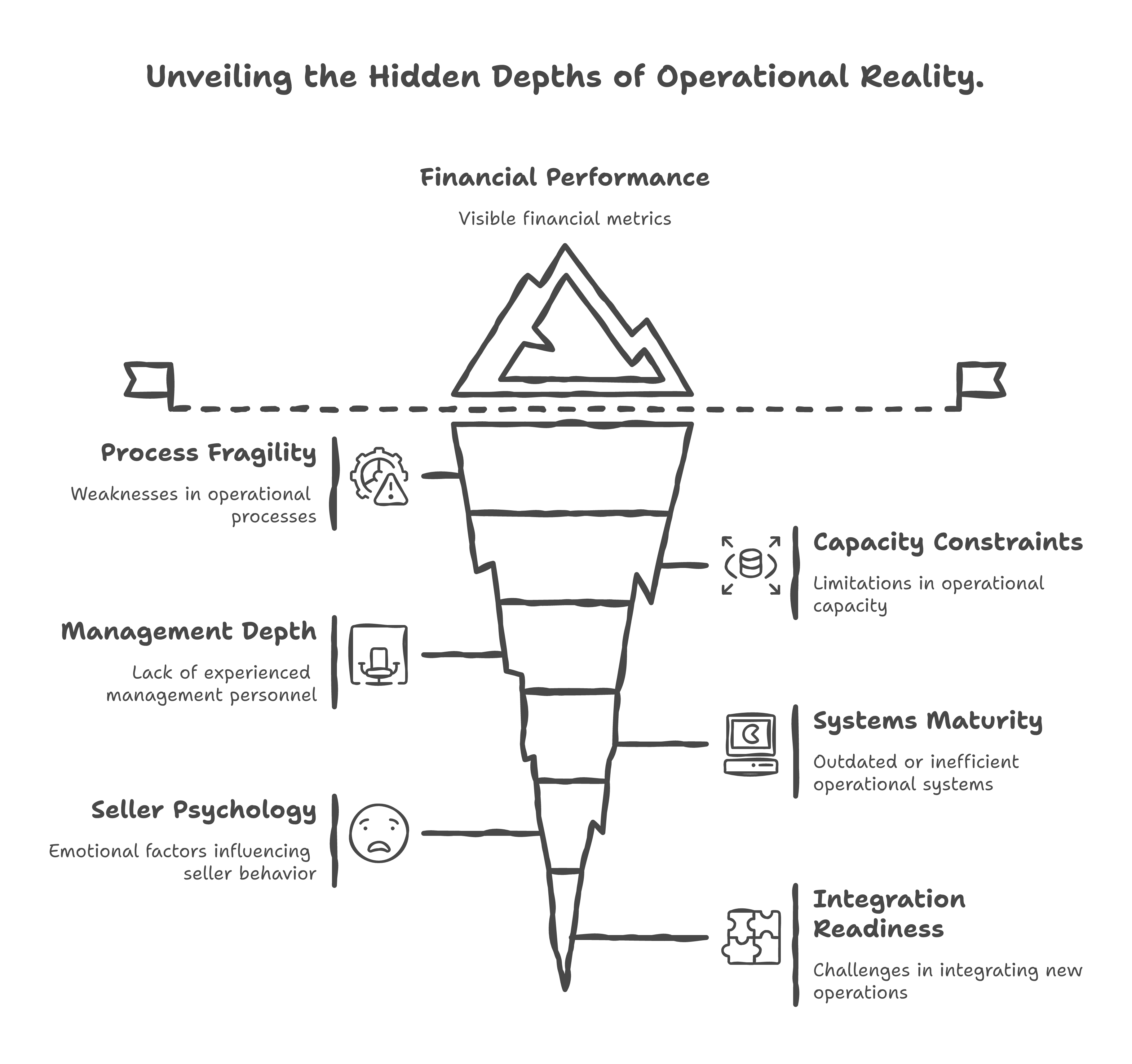

The Six Things Operational DD Actually Reveals

The lack of a standard ODD framework is part of what makes it easy to skip. Here’s what a real operational assessment surfaces that financial diligence won’t.

Process fragility. How much of the business’s performance depends on specific individuals knowing things that aren’t written down? Every business has tribal knowledge. ODD maps where it concentrates and what happens if those people leave.

Capacity reality. The value creation plan assumes the business can grow at a certain pace. ODD asks whether the team, the systems, and the workflows can actually absorb that growth without breaking. Most plans assume available bandwidth. Most teams don’t have it.

Management depth. Not whether the management team is competent — financial diligence might pick that up. But whether there’s a second tier of leadership that can execute independently when the CEO is in acquisition mode or dealing with the inevitable integration chaos.

Systems maturity. Not whether the systems are running, but whether they’re generating the operational data that lets you measure improvement post-close. Month 4 post-acquisition, you should be able to tell if things are getting better. Plenty of operators can’t.

Integration readiness. For add-on strategies, this is especially critical. Can this platform absorb another business? Does it have the back-office infrastructure, the reporting cadence, the process documentation to onboard a new entity without collapsing under the weight of two sets of everything?

Revenue stream economics. Which customers, products, or service lines are actually generating the margin the model assumes? Consolidated EBITDA hides this. Per-unit P&Ls reveal it. The mechanics of cascading those unit economics into operating decisions is a post-close discipline — but you need to know the economics exist before you close.

The Firms That Win Treat ODD as Table Stakes

If roughly two-thirds of the old return model is gone and operational value creation is what’s left, then operational assessment isn’t optional anymore. It’s the prerequisite — and generating return from operations requires knowing what you’re integrating before you close, not six months after.

The good news is operational DD isn’t a six-figure engagement. A structured operational assessment runs $30K–50K. Against the cost of six months of post-close confusion, misallocated resources, and a management team running at capacity on problems they didn’t know existed until after they owned them — that’s not an expense. It’s the cheapest insurance in the deal.

This is also where analytics and operational data strategy fit into the picture — not as a post-close technology project, but as a pre-close question. Can you actually see what this business is doing at the unit level? If the answer is no, that’s material to the value creation plan. ODD answers it before you’re committed.

A PE operator described the consequence plainly: “Everything financial looked perfect but the human capital side fell apart post-close.” The financial side looked perfect because it was assessed. The human capital side fell apart because it wasn’t.

Deal assumptions and operational reality diverge. They do it every time there’s a gap between what diligence validated and what the business actually needs to improve. The firms building ODD into their process are closing that gap before close. The ones that aren’t are discovering it on the other side.

The Question Every PE Firm Needs to Answer

The era of financial engineering is over. That’s what the data shows. The era of operational value creation is here.

Most diligence processes aren’t built for it. They were built for a different return model — excellent at validating financial stories and identifying legal and tax risk, not built to answer whether the business can actually execute.

The firms that add operational assessment to their standard diligence stack — not as a nice-to-have but as a gate — have a structural advantage that compounds over the next decade. The ones that don’t are buying spreadsheets. And in the current environment, that’s an increasingly expensive habit.

Alex Escoriaza helps PE firms and operating partners figure out what good looks like before and after the transaction. If you’re building out your operational diligence capability or need an operational assessment on an active deal, reach out.