Growth Is the Hardest Part of PE Value Creation

The industry tells a story where cost-cutting is the blunt instrument and growth is the sophisticated lever. Smart operators run the growth play. Lesser operators wield the axe. If your growth plan is stuck, the implicit message is that you’re doing it wrong — because growth is supposed to be the exciting part, the energizing one.

Operators experience it the opposite way. Cost-cutting feels hard because it’s emotionally hard: layoffs, restructuring, conflict, uncomfortable conversations. Growth feels exciting because it’s energizing: new products, new markets, momentum. Most people walk in assuming growth will be easier on the merits and just harder to start.

Mechanically, the opposite is true. If you’re a portco operator wondering why your growth plan is stuck while the cost work executed clean, you’re not failing. You’re doing the genuinely harder problem.

Why Cost-Cutting Is Mechanically Straightforward

Cost-cutting has a finite playbook. The list of expenses is bounded — payroll, vendors, real estate, software, T&E, freight, materials. You can put it on a page. You can attack it line by line. You can benchmark every category against companies your size in your industry and know within a few percentage points where you should land.

The math is predictable. Cut $X, save $X. Maybe you lose some second-order revenue if you cut the wrong salesperson, but the first-order effect is direct, immediate, and visible in the P&L next month. You control the inputs almost entirely.

Even the emotionally hard parts have a script. Severance packages, comms plans, transition support, who walks who out of the building — all of it has been done thousands of times. There’s discipline required, and empathy required for the people involved. But mechanically, you know exactly what to do.

That’s not a knock on people who do this work well. Cost discipline is genuinely valuable. The point is that the uncertainty around it is low. You’re solving a closed-form problem with a known answer.

Growth is not that.

Why Growth Is Genuinely Hard

In growth, almost every variable that matters is outside your control. Will customers want the new product? Will the market move with you or away from you? Will your competitor cut prices the week your launch goes live? Will the salesperson you just hired actually close? Will the channel partner deliver, or treat you as their tenth priority?

You can do everything right and still get a bad outcome. You can do half of it wrong and stumble into a great one. The signal-to-noise ratio is awful for the first six months, sometimes the first eighteen. You’re navigating uncertainty, not executing a checklist.

Andrew Joy, partner at Hidden Harbor Capital Partners, frames the whole thing in five words: “Strategy easy, execution hard.” Anyone can write the growth plan. The plan is roughly the same plan everyone else would write — increase service mix, M&A in adjacent categories, lean out the cost structure, improve working capital. Ask any PE professional and you get the same conclusions. The difference between firms that compound returns and ones that don’t isn’t the strategy. It’s the execution.

And growth is where execution is hardest, because execution in growth means executing in uncertainty. You’re not following a playbook. You’re building one as you go.

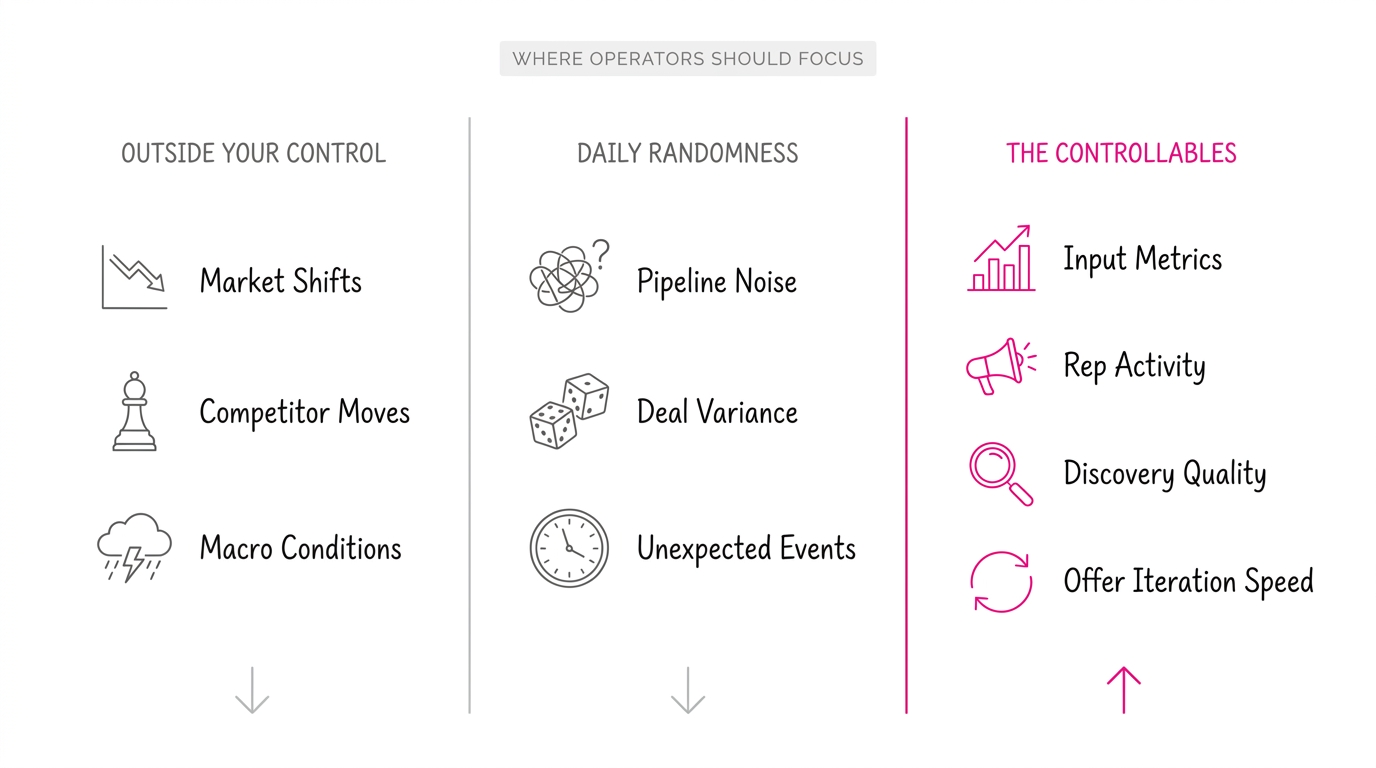

That framing sounds obvious until you sit inside a stalled growth initiative and watch how often operators miss the distinction. They take credit for randomness when things go well. They blame randomness when things go badly. They miss the actual controllables — pipeline conversion, rep activity, discovery quality, iteration speed on the offer — because they’re busy reacting to noise.

The Two-Layer Argument

Pair the two voices and you get the whole picture.

Ben Gaw, head of portfolio operations at Cross Rapids Capital, puts it bluntly on a recent BluWave podcast: “Growth is the hardest. Cutting costs is straightforward — anyone can cut.” The same thesis from the PE-partner level: strategy is commodity, execution is the moat. Two vantage points, one diagnosis.

If you accept both, the implication is uncomfortable: most PE value creation lives or dies on the part that’s hardest to plan, hardest to predict, and hardest to coach from a board seat. And the part the industry talks about most — the deck, the thesis, the value creation plan — is the relatively easier piece.

Joy goes one step further: “A successful private equity investment is all just about timing and your executive teams. That explains 95% of if you get a good team and the timing is at least okay to good.”

Read that twice. If 95% of PE success is team plus timing, then growth capability — which depends almost entirely on team quality and willingness to execute through uncertainty — is the whole game. We’ve made the team-as-EBITDA-engine version of this argument before — knowing who creates the EBITDA is the human-capital corollary to that claim. Cost-cutting is necessary. It’s not sufficient. Nobody compounds returns over a five-year hold by being world-class at expense management.

What This Means for Operators

If you’re in the messy middle of a growth push and it feels harder than the cost work did, you’re not behind. You’re on the harder problem.

A few implications fall out of that.

Stop measuring growth like cost work. Cost-cutting gives you clean weekly progress. Headcount down, vendor spend down, run rate visible by Friday. Growth doesn’t work that way. The lag between input and outcome is months, not weeks. And most portcos compound the problem: the leading indicators that precede the outcome — pipeline conversion rates, rep activity volume, offer iteration cadence — aren’t instrumented at all. You’re not just navigating uncertainty. You’re navigating it without the partial visibility you could have. If you’re grading yourself on the same cadence you graded cost work, you’ll fire people and pivot programs that were two weeks from breaking through. Build a cadence that matches the actual feedback loop — and instrument the inputs before you start grading the outputs.

Resource growth like the harder problem it is. Most portcos under-invest in growth capability relative to cost discipline. CFO function is sacred. RevOps is whatever the head of sales has time for between quotas. Marketing is a line item. Pricing analytics is a project that gets approved twice and started zero times. If growth is genuinely the hardest part of value creation and you’re staffing it as the side hustle, the math doesn’t work.

Pick speed over perfection. Gaw again: “Speed over perfection in turnarounds. Waiting for the perfect plan means you’ve already lost.” This applies double to growth. The perfect launch doesn’t exist. The perfect ICP doesn’t exist. The perfect product doesn’t exist. You will course-correct three times in the first six months no matter how careful you are upfront. The faster you start, the more iterations you get inside the hold period.

Separate the controllables from the noise. Most growth post-mortems blame the wrong things. Q3 missed because the market got soft. Q4 missed because a competitor moved. Q1 missed because the new rep ramped slow. All of those are partially true and entirely unhelpful. The useful question is: of the things we actually controlled, what did we do well and what did we do badly? That’s the only conversation that compounds into a better Q2 — and it’s where a real metrics cascade earns its keep, by pushing the controllables down to the people who actually move them.

Expect the volatility. One of the more useful operating principles in growth work: things are never as good or as bad as they appear in the moment. Growth has higher highs and lower lows than cost work. The pipeline that looked dead in March books $4M in May. The pipeline that looked stacked in May closes $400K. Make every staffing decision based on the most recent two-week trend and you’ll burn out your team and miss the underlying signal.

What Nobody Warns Operators About

Operators in growth mode don’t get the clean exit cost-cutters get. There’s no “we hit the number” moment six weeks in. Growth requires resilience through long stretches where you can’t tell whether you’re winning or losing — where the data is noisy, the market is moving, and customer feedback is mixed.

Nobody tells you going in: you won’t know how resilient you are until the options run out — which is exactly the position growth work puts operators in more often than the deck suggests.

Growth doesn’t grade itself in a quarter. Sometimes not in a year. You’re being asked to invest belief, energy, and judgment into work that won’t pay you back on a predictable schedule, while the cost-cutting workstream next door is publishing weekly wins.

If you’re feeling that gap, you’re not soft. You’re paying attention.

The PE industry doesn’t talk about this enough. The decks celebrate growth wins and audit the cost work. The reality is that the team running the growth bet is doing the harder job under more uncertainty with less reinforcement, and the system mostly pretends otherwise.

The Real Test

Deeply unfashionable in a market that sells hacks, the actual answer from partners who’ve watched enough deals close and fall apart: sustained, unglamorous effort with no shortcut. No system, no framework, no life hack. But it’s the answer that matches the reality of growth work. Cost-cutting has a finite playbook. Growth requires sustained, unglamorous, iterative effort under uncertainty — and a team that doesn’t quit when the first three swings miss.

Two questions to sit with this week:

What’s your actual growth hypothesis — written down, falsifiable, with a real test you’ll run by month-end? Not the value creation plan. The thing you’re actually betting on.

And: if you accepted that growth is the hardest part, not the easiest, would you resource it differently than you do today?

The cost work will close on schedule. It almost always does. The growth work is where the hold period gets won or lost — and where most operators are quietly carrying more weight than the system gives them credit for.

Alex Escoriaza helps PE-backed companies and their portcos build the instrumentation layer between growth activity and growth outcomes — making the controllables visible before the post-mortem, with the data you already have. Reach out.