The DD Type PE Firms Skip (And Pay For Later)

There are four types of due diligence PE firms run on every deal. Financial. Commercial. Legal. Tax. Sometimes insurance. The deal team checks the books, checks the market, checks the contracts, checks the exposure.

Nobody checks how the business runs.

That’s how you end up buying a $20M problem disguised as a $20M opportunity.

The DD Stack Has a Hole in It

Walk through a standard deal process. Quality of Earnings validates the financials — is the EBITDA real, are the adjustments defensible? Commercial due diligence validates the market — is the TAM reasonable, are customers sticky? Legal DD validates contracts and liabilities. Tax DD validates the structure.

Notice what’s missing.

None of those workstreams answer a basic question: Can this business execute the value creation plan you’re underwriting? Diligence validates the spreadsheet, not how the business works.

The QofE tells you EBITDA margins are 18%. It doesn’t tell you those margins depend on one machine operator who’s been running the CNC line for 22 years and is planning to retire. The CDD tells you the market is growing 7% annually. It doesn’t tell you production capacity is already at 93% utilization and the floor layout can’t accommodate a second shift.

This is operational due diligence — ODD — and it’s the gap in virtually every lower middle market deal process. If you’ve read about what PE’s Day 1 playbook misses, this is the pre-close version of the same problem.

Why Operational DD Gets Skipped

The gap isn’t accidental. There are structural reasons ODD doesn’t happen, and they’re all fixable once you see them.

Deal teams want to close. This is the uncomfortable one. As one PE professional put it: “Too many finance deal guys don’t know anything about real business or operations besides what exists in a spreadsheet.” Harsh, but there’s truth in it. Deal teams are evaluated on closed transactions. ODD findings create friction — they surface problems that complicate timelines. Every additional workstream is another potential reason to re-trade or walk away. If your incentive is to close, you’re not looking for reasons not to.

There’s no standard framework. Financial DD has a playbook. Every QofE provider runs the same core analysis. Legal DD has a checklist everyone agrees on. Operational DD? No Big Four practice owns this category. No standard deliverable. No agreed-upon scope. When something doesn’t have a template, it doesn’t get ordered.

The “we’ll fix it post-close” assumption. This one is pervasive. The thesis goes: We know the operations are rough. That’s the value creation opportunity. We’ll optimize after we own it. The problem? You’re sizing the “fix it” budget based on zero operational data. You’re guessing how broken things are. Sometimes you guess right. Often you don’t.

What ODD Reveals That Financial DD Can’t

Here’s what you miss when you skip the operational assessment. These show up in month three or month six post-close, when it’s too late to renegotiate.

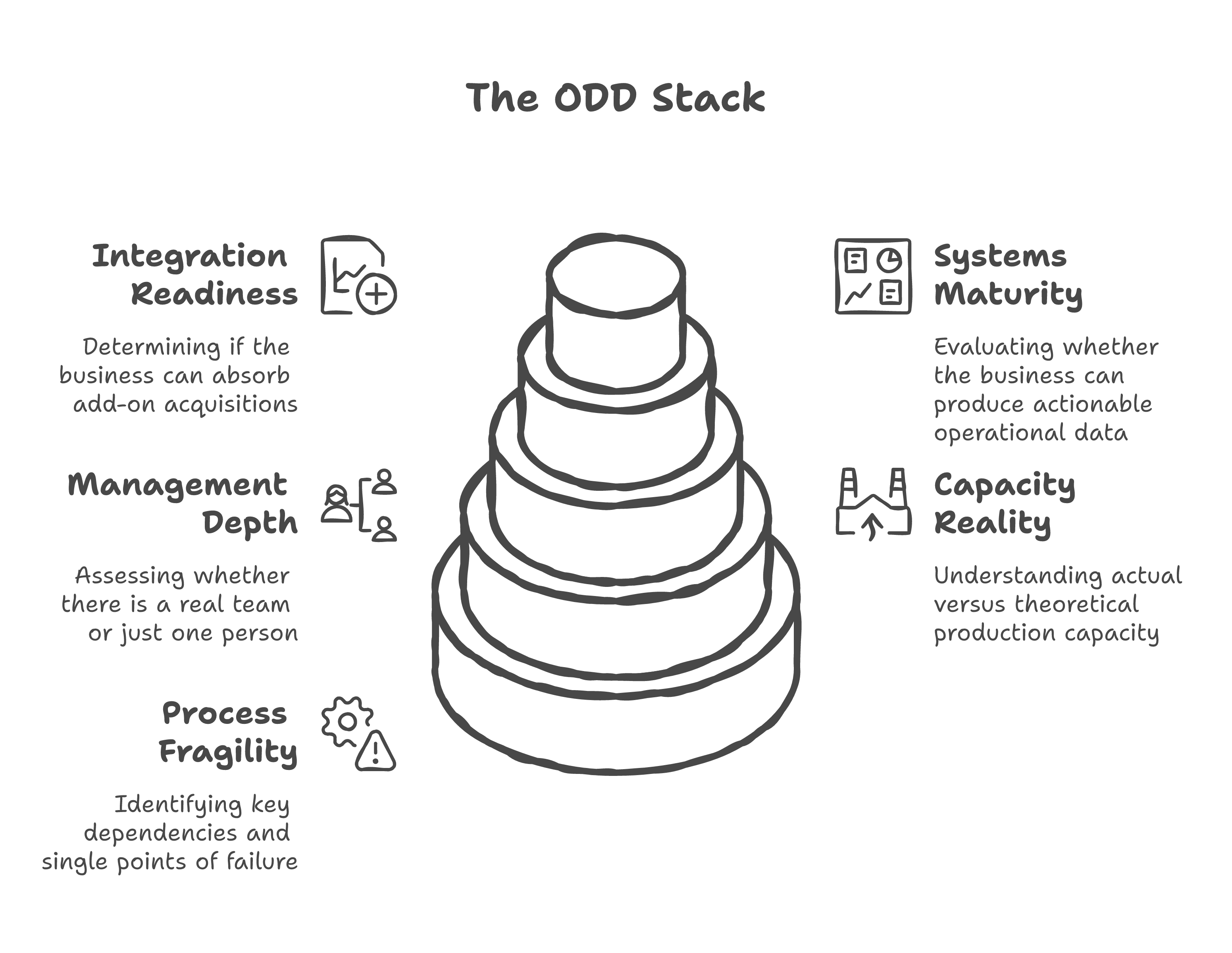

Process fragility. Every business has dependencies that don’t appear on financial statements. The one supplier providing a critical component with no backup. The one technician certified to operate the coating line. The one customer representing 35% of revenue who renegotiates every year. QofE shows you the revenue. It doesn’t show you how fragile the revenue-generating machinery is.

Capacity reality versus the model. The deal model assumes 15% revenue growth in Year 2. Has anyone checked whether the facility can handle it? Theoretical capacity and actual capacity are different numbers. Actual capacity accounts for changeover time, maintenance windows, quality rework, seasonal labor shortages. Imagine underwriting a manufacturing acquisition at $40M and discovering post-close that hitting your Year 2 target requires a $3M capital expenditure the model never contemplated.

Management depth. Is there a real leadership team, or is one person doing everything? This is especially acute in founder-led businesses — the founder might be CEO, head of sales, and de facto plant manager. Financial statements don’t tell you that. An org chart might exist on paper, but actual decision-making authority often tells a different story. This is the same founder transition problem that derails post-close plans — the difference is that ODD catches it before you wire the funds.

Systems maturity. Can the business produce operational data? Not financial data — the accountant handles that. Production yield by line. Labor cost per unit. On-time delivery rates. Customer acquisition cost by channel. If the business can’t generate these numbers today, your post-close analytics buildout just got more expensive and slower than your 100-day plan assumed. Existence ≠ utility. A system can exist and produce nothing you can act on.

Integration readiness. This matters most for roll-ups. If you’re planning to acquire three more companies in the same vertical over the next 24 months, you need a platform that can absorb them. Can this first acquisition’s processes be standardized and replicated? Or are they so bespoke that every add-on requires custom integration? That question has seven-figure implications, and nobody’s asking it pre-close.

The Cost of Not Asking

Here’s a pattern that plays out more than the industry admits.

Everything financial looked perfect. Revenue growing, margins healthy, QofE came back clean. Deal closes. Then the human capital side falls apart. 35% turnover within 18 months. The leadership team the acquirer underwrote isn’t the team running the business by month six. New CEO, new CFO, new CRO — all within the first year.

Each replacement costs real money. Recruiting fees. Ramp time. Strategic drift while the seat is empty. By the time you’ve cycled through three C-suite hires, you’ve spent $300K to $500K in direct costs and lost a year of value creation momentum. A $40K to $75K ODD engagement would have revealed what a $500K talent replacement cycle eventually proved.

And that’s just the people dimension. Add the capital expenditure surprises, the supplier concentration risk nobody flagged, the IT systems that need ripping out. The tab compounds fast.

You cannot run a business from the financial statements. They tell you what happened. They don’t tell you why, and they don’t tell you whether it will keep happening under new ownership.

What a Real Operational DD Should Cover

If you’re running a deal on a manufacturing or services business, here’s what the ODD workstream should include. Not as a checklist exercise — as an assessment by someone who understands operations.

Floor walk and process mapping. Physical observation, not a conference room presentation. Walk the floor. Watch the workflow. Where are the bottlenecks? Where does work-in-process pile up? Where are people working around the system instead of through it? An industrial engineer spends a day on the floor and sees things a deal team never will.

Equipment and capacity. Age and condition of critical assets. Maintenance backlog. Deferred capex that will hit the P&L in Year 1. These aren’t financial questions — they’re operational questions with financial consequences.

Labor analysis. Skill concentration, tenure distribution, compensation benchmarking. If three people possess 80% of the institutional knowledge and they’re all over 55, that’s a succession risk the deal model should price in.

Systems audit. What technology exists, what’s being used, and what’s the gap between current state and what the value creation plan requires? This is where you move beyond the spreadsheets and find the real bottlenecks. Many businesses pass the “systems exist” test during diligence but fail the “systems work” test on day one post-close.

Supplier and customer concentration. Financial DD flags revenue concentration. ODD goes deeper: What does the relationship look like? Are there contracts, or handshake agreements? What happens if the key supplier raises prices 15%? Is there an alternative source qualified and ready?

Scalability stress test. Can this business grow 30% without breaking? Where will it break first? What investment is required to build capacity ahead of the growth curve? The deal model assumes growth. ODD tests whether the operations can deliver it.

Before You Sign the LOI

Ask yourself one question: Do you know how this business runs?

Not how the P&L says it runs. Not how the management presentation describes it. How it runs. What happens on the floor at 6 AM when the first shift starts. What breaks when the senior technician calls in sick. How orders flow from intake to delivery. Where the real constraints sit.

If you can’t answer those questions before you close, you’re underwriting a spreadsheet. And spreadsheets don’t run businesses.

This is where deal assumptions and operational reality diverge. The deal model works on paper. The question is whether the operations can make it work in practice. The firms that answer that question before close — instead of discovering the answer after — are the ones that hit their value creation plans.

Alex Escoriaza helps PE-backed companies figure out what good looks like — turning operational ambiguity into measurable clarity. If you’re evaluating a deal and need to understand what’s really happening behind the financials, let’s talk.